Page 139 - ENVISAGE - Souvenir 2024 - Flip Book

P. 139

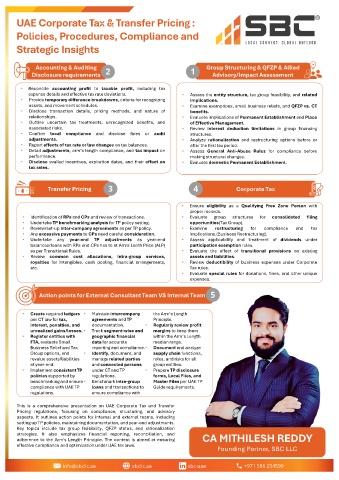

UAE Corporate Tax & Transfer Pricing :

Policies, Procedures, Compliance and

Strategic Insights

Accounting & Auditing 2 1 Group Structuring & QFZP & Allied

Disclosure requirements Advisory/Impact Assessment

• Reconcile accounting profit to taxable profit, including tax

expense details and effective tax rate deviations. • Assess the entity structure, tax group feasibility, and related

• Provide temporary difference breakdowns, criteria for recognizing implications.

assets, and movement schedules. • Examine exemptions, small business reliefs, and QFZP vs. CT

• Disclose transaction details, pricing methods, and nature of benefits.

relationships. • Evaluate implications of Permanent Establishment and Place

• Outline uncertain tax treatments, unrecognized benefits, and of Effective Management.

associated risks. • Review interest deduction limitations in group financing

• Confirm local compliance and disclose fines or audit structures.

adjustments. • Analyze rationalization and restructuring options before or

• Report effects of tax rate or law changes on tax balances. after the first tax period.

• Detail adjustments, arm’s length compliance, and tax impact on • Assess General Anti-Abuse Rules for compliance before

performance. making structural changes.

• Disclose availed incentives, expiration dates, and their effect on • Evaluate domestic Permanent Establishment.

tax rates.

Transfer Pricing 3 4 Corporate Tax

• Ensure eligibility as a Qualifying Free Zone Person with

proper records.

• Identification of RPs and CPs and review of transactions. • Evaluate group structures for consolidated filing

• Undertake TP benchmarking analysis for TP policy setting. opportunities(Tax Group).

• Review/set-up inter-company agreements as per TP policy. • Examine restructuring for compliance and tax

• Any excessive payments to CPs need careful consideration. implications.(Business Restructuring).

• Undertake any year-end TP adjustments as year-end • Assess applicability and treatment of dividends under

balances/loans with RPs and CPs has to at Arms Lenth Price (ALP) participation exemption rules.

as per Transitional Rules. • Evaluate the effect of transitional provisions on existing

• Review common cost allocations, Intra-group services, assets and liabilities.

royalties for Intangibles, cash pooling, financial arrangements, • Review deductibility of business expenses under Corporate

etc. Tax rules.

• Evaluate special rules for donations, fines, and other unique

expenses.

Action points for External Consultant Team VS Internal Team 5

• Create required ledgers • Maintain intercompany the Arm’s Length

per CT law for tax, agreements and TP Principle.

interest, penalties, and documentation. • Regularly review profit

unrealized gains/losses. • Track segment-wise and margins to keep them

• Register entities with geographic financial within the Arm’s Length

FTA, evaluate Small data for accurate median range.

Business Relief and Tax reporting and compliance.• Document and analyze

Group options, and • Identify, document, and supply chain functions,

revalue assets/liabilities manage related parties roles, and risks for all

at year-end. and connected persons group entities.

• Implement consistent TP under CT and TP • Prepare TP disclosure

policies supported by regulations. forms, Local Files, and

benchmarking and ensure • Benchmark intra-group Master Files per UAE TP

compliance with UAE TP loans and transactions to Guide requirements.

regulations. ensure compliance with

This is a comprehensive presentation on UAE Corporate Tax and Transfer

Pricing regulations, focusing on compliance, structuring, and advisory

aspects. It outlines action points for internal and external teams, including

setting up TP policies, maintaining documentation, and year-end adjustments.

Key topics include tax group feasibility, QFZP status, and rationalization

strategies. It also emphasizes financial reporting, reconciliation, and www.icaidubai.org 139

adherence to the Arm's Length Principle. The content is aimed at ensuring CA MITHILESH REDDY

effective compliance and optimization under UAE tax laws. Founding Partner, SBC LLC

UAE Transfer Pricing Impact Assessment

42 nd ANNUAL INTERNATIONAL 42 nd ANNUAL INTERNATIONAL

$5 Trillion $5 Trillion

Economy CONFERENCE 2024-25 CONFERENCE 2024-25 Economy

PROFESSION, BHARAT & WORLD ECONOMY

PROFESSION, BHARAT & WORLD ECONOMY [email protected] sbcllc.ae sbc-uae PR OFESSION, BHARA 254599 LD EC ONOM Y

PR

OR

T & W

+971 586

LD EC

ONOM

Y

OFESSION, BHARA

T & W

OR